Research on Macroeconomic Nonlinear Forecasting Based on DCL-MHA Collaborative Architecture and Residual Gating Mechanism

Keywords:

Macroeconomic Forecasting, DCL-MHA Architecture, LSTM-GRU, Residual Gating, Nonlinear ModelingAbstract

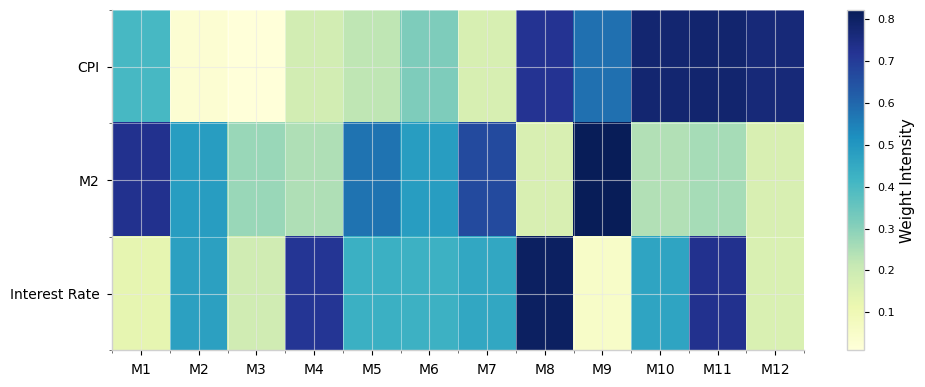

To address non-linear fluctuations and error accumulation in macroeconomic forecasting, this paper proposes the DCL-MHA framework, a dual-track architecture integrating an LSTM_Temporal_Model with a Residual Gating chain. By simulating econometric error correction logic, this design enables context-aware dynamic weighting and high-fidelity feature preservation across multi-dimensional economic indicators. Empirical research conducted on 2021–2024 GDP data demonstrates that the proposed model achieves a substantial breakthrough in accuracy with a 1.2% MAPE, representing a 50% improvement over traditional ARIMA, VAR, and standalone LSTM models. Furthermore, in T+12 long-range stress tests, the framework successfully suppressed the RMSE from over 8.0 to approximately 4.0, effectively doubling the forecasting stability. Heatmap analysis of dynamic weights further confirms that the Residual Gating mechanism adaptively adjusts focus across variables such as CPI, M2, and interest rates based on shifts in the economic environment. This study proves that the DCL-MHA architecture provides a high-precision, high-stability decision-support solution for digital macro-control and economic risk early warning.

References

Diebold, F. X., & Mariano, R. S. (2002). Comparing predictive accuracy. Journal of Business & economic statistics, 20(1), 134-144.

LeCun, Y., Bengio, Y., & Hinton, G. (2015). Deep learning. nature, 521(7553), 436-444.

Bengio, Y., Simard, P., & Frasconi, P. (1994). Learning long-term dependencies with gradient descent is difficult. IEEE transactions on neural networks, 5(2), 157-166.

Graves, A. (2012). Long short-term memory. Supervised sequence labelling with recurrent neural networks, 37-45.

Cho, K., Van Merriënboer, B., Gulçehre, Ç., Bahdanau, D., Bougares, F., Schwenk, H., & Bengio, Y. (2014, October). Learning phrase representations using RNN encoder–decoder for statistical machine translation. In Proceedings of the 2014 conference on empirical methods in natural language processing (EMNLP) (pp. 1724-1734).

Bok, B., Caratelli, D., Giannone, D., Sbordone, A. M., & Tambalotti, A. (2018). Macroeconomic nowcasting and forecasting with big data. Annual Review of Economics, 10(1), 615-643.

Guidotti, R., Monreale, A., Ruggieri, S., Turini, F., Giannotti, F., & Pedreschi, D. (2018). A survey of methods for explaining black box models. ACM computing surveys (CSUR), 51(5), 1-42.

Wang, X., & Guo, D. (2026). Adaptive-Gated Spiking Neural Networks with Memristive Crossbars for Real-Time Athlete Injury Prediction. International Journal of Advanced AI Applications, 2(1), 1-16.

Athey, S. (2018). The impact of machine learning on economics. In The economics of artificial intelligence: An agenda (pp. 507-547). University of Chicago Press.

Ning, J., Huang, W., Ma, H., Wu, M., Hu, Y., & Shi, D. (2026). A Partition Collaborative Prediction Method for Wind Farm Cluster Based on Multi–Scale Component Reconstruction and Fusion Technology. Journal of Electrical Engineering & Technology, 1-17.

Mullainathan, S., & Spiess, J. (2017). Machine learning: an applied econometric approach. Journal of Economic Perspectives, 31(2), 87-106.

Madhulatha, T. S., & Ghori, D. M. A. S. (2025). Deep neural network approach integrated with reinforcement learning for forecasting exchange rates using time series data and influential factors. Scientific reports, 15(1), 29009.

Guo, D., Li, Z., & Tao, T. (2025). Bio-Inspired Adaptive Dynamic Attention: An Empirically Driven AI Framework for Human–Machine Coaching in Team Collaborative Decision-Making. International Journal of Advanced AI Applications, 1(8), 22-38.

Khan, R., & Jie, W. (2025). Using the TSA-LSTM two-stage model to predict cancer incidence and mortality. Plos one, 20(2), e0317148.

Hosseini, S. A., Grimaccia, F., Niccolai, A., & Trimarchi, S. (2025). Pattern-Based Feature Extraction for Improved Deep Learning in Financial Time Series Classification. IEEE Access.

Yin, H., Chen, Y., Zhou, J., Xie, Y., Wei, Q., & Xu, Z. (2025). A probabilistic deep learning approach to enhance the prediction of wastewater treatment plant effluent quality under shocking load events. Water Research X, 26, 100291.

Ren, Y., Liu, X., & Zhu, Y. (2025). The role of renewable energy investment in energy economic efficiency under the “dual carbon” drive. International Review of Economics & Finance, 104553.

Yadav, H., & Thakkar, A. (2024). NOA-LSTM: An efficient LSTM cell architecture for time series forecasting. Expert Systems with Applications, 238, 122333.

Das, N., Sadhukhan, B., Ghosh, R., & Chakrabarti, S. (2024). Developing hybrid deep learning models for stock price prediction using enhanced Twitter sentiment score and technical indicators. Computational Economics, 64(6), 3407-3446.

Kashyap, A. K., & Stein, J. C. (2023). Monetary policy when the central bank shapes financial-market sentiment. Journal of Economic Perspectives, 37(1), 53-75.

Uribe, M. D. R., Coe, M. T., Castanho, A. D., Macedo, M. N., Valle, D., & Brando, P. M. (2023). Net loss of biomass predicted for tropical biomes in a changing climate. Nature Climate Change, 13(3), 274-281.

Abdi, A. H., Ahmed, A. M., & Khalif, A. A. (2025). Agricultural market integration: investigating the impacts of trade openness and climate change on food production in Somalia. Cogent Food & Agriculture, 11(1), 2596345.

Stover, O., Karve, P., & Mahadevan, S. (2025). Periodic Regression in the Principal Component Space for Multivariate, Multi‐Horizon, Probabilistic Forecasting. Journal of Forecasting.

Alhussan, A. A., El-Kenawy, E. S. M., Khafaga, D. S., Alharbi, A. H., & Eid, M. M. (2025). Groundwater resource prediction and management using comment feedback optimization algorithm for deep learning. IEEE Access.

Wang, Z., & Liu, H. (2026). Artificial intelligence and the historical performance expectation gap: Evidence from the moderating role of monetary easing. Economic Analysis and Policy.

Ibrahimov, O., Vancsura, L., & Parádi-Dolgos, A. (2025). The impact of macroeconomic factors on the firm’s performance—Empirical analysis from Türkiye. Economies, 13(4), 111.