A Review of Stock Index Forecasting Methods from ARIMA to Time-Series Foundation Models

Keywords:

Stock Index Forecasting, Financial Time Series, Deep Learning, Transformers, State Space Models, Foundation ModelsAbstract

Stock index forecasting has evolved from linear statistical baselines to hybrid deep neural architectures and, more recently, to large-scale time-series foundation models. This review synthesizes the development path represented by the supplied literature, covering ARIMA, GARCH, and VAR models; classical machine learning methods such as random forests and boosting; recurrent, convolutional, and attention-based deep learning models; decomposition-driven hybrids; selective state space models; and emerging large-model approaches for time-series analysis. The review is organized around the inductive biases that different model families impose on financial data, with special attention to nonstationarity, volatility clustering, multimodal information fusion, and distribution shift. Compared with generic forecasting domains, stock index prediction places stronger demands on robustness, interpretability, and economic usefulness because signal-to-noise ratios are low and model errors can be magnified by trading decisions. Across the surveyed studies, no single architecture dominates all settings; instead, performance depends on how well a method aligns with data frequency, exogenous information, market regime, and evaluation objective. The review concludes that future progress is likely to come from financially informed hybrid systems, stronger benchmark design, and better integration between domain-specific supervision and foundation-model pretraining.

References

Bai, S., Kolter, J. Z., & Koltun, V. (2018). An empirical evaluation of generic convolutional and recurrent networks for sequence modeling. arXiv preprint arXiv:1803.01271.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307–327. https://doi.org/10.1016/0304-4076(86)90063-1

Breiman, L. (2001). Random forests. Machine Learning, 45(1), 5–32. https://doi.org/10.1023/A:1010933404324

Cao, D., Jia, F., Arik, S. O., Pfister, T., Zheng, Y., Ye, W., & Liu, Y. (2024). TEMPO: Prompt-based generative pre-trained transformer for time series forecasting. In Proceedings of the International Conference on Learning Representations (ICLR).

Chen, S.-A., Li, C.-L., Arik, S. O., Yoder, N. C., & Pfister, T. (2023). TSMixer: An all-MLP architecture for time series forecasting. Transactions on Machine Learning Research.

Cho, K., van Merrienboer, B., Gulcehre, C., Bahdanau, D., Bougares, F., Schwenk, H., & Bengio, Y. (2014). Learning phrase representations using RNN encoder-decoder for statistical machine translation. In Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing (pp. 1724–1734). https://doi.org/10.3115/v1/D14-1179

Das, A., Kong, W., Leach, A., Mathur, S., Sen, R., & Yu, R. (2023). Long-term forecasting with TiDE: Time-series dense encoder. arXiv preprint arXiv:2304.08424.

Das, A., Kong, W., Sen, R., & Zhou, Y. (2024). A decoder-only foundation model for time-series forecasting. In Proceedings of the 41st International Conference on Machine Learning (Vol. 235, pp. 10148–10167). PMLR.

Fischer, T., & Krauss, C. (2018). Deep learning with long short-term memory networks for financial market predictions. European Journal of Operational Research, 270(2), 654–669. https://doi.org/10.1016/j.ejor.2017.11.054

Freund, Y., & Schapire, R. E. (1997). A decision-theoretic generalization of on-line learning and an application to boosting. Journal of Computer and System Sciences, 55(1), 119–139. https://doi.org/10.1006/jcss.1997.1504

Ge, Q. (2025). Enhancing stock market forecasting: A hybrid model for accurate prediction of S&P 500 and CSI 300 future prices. Expert Systems with Applications, 260, Article 125380. https://doi.org/10.1016/j.eswa.2024.125380

Gu, A., & Dao, T. (2023). Mamba: Linear-time sequence modeling with selective state spaces. arXiv preprint arXiv:2312.00752.

He, Z., Zhang, H., & Por, L. Y. (2024). A comparative study on deep learning models for stock price prediction. In Image Processing, Electronics and Computers: Advances in Transdisciplinary Engineering. IOS Press. https://doi.org/10.3233/ATDE240502

Hochreiter, S., & Schmidhuber, J. (1997). Long short-term memory. Neural Computation, 9(8), 1735–1780. https://doi.org/10.1162/NECO.1997.9.8.1735

Hoseinzadeh, E., & Haratizadeh, S. (2019). CNNpred: CNN-based stock market prediction using a diverse set of variables. Expert Systems with Applications, 129, 273–285. https://doi.org/10.1016/j.eswa.2019.03.029

Ilbert, R., Odonnat, A., Feofanov, V., Virmaux, A., Paolo, G., Palpanas, T., & Redko, I. (2024). SAMformer: Unlocking the potential of transformers in time series forecasting with sharpness-aware minimization and channel-wise attention. In Proceedings of the 41st International Conference on Machine Learning (Vol. 235, pp. 20924–20954). PMLR.

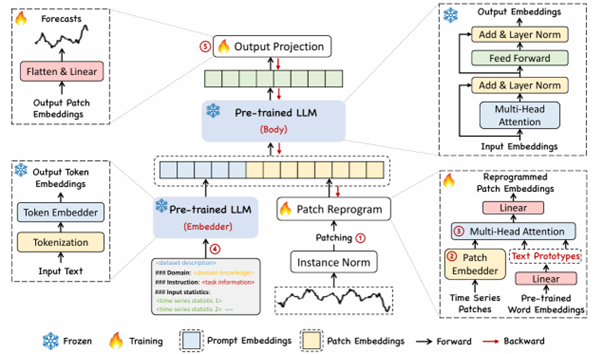

Jin, M., Wang, S., Ma, L., Chu, Z., Zhang, J. Y., Shi, X., Chen, P.-Y., Liang, Y., Li, Y.-F., Pan, S., & Wen, Q. (2024). Time-LLM: Time series forecasting by reprogramming large language models. In Proceedings of the International Conference on Learning Representations (ICLR).

Kim, T., Kim, J., Tae, Y., Park, C., Choi, J.-H., & Choo, J. (2022). Reversible instance normalization for accurate time-series forecasting against distribution shift. In Proceedings of the Tenth International Conference on Learning Representations (ICLR).

Li, S., Tang, G., Chen, X., et al. (2024). Stock index forecasting using a novel integrated model based on CEEMDAN and TCN-GRU-CBAM. IEEE Access, 12, 122524–122543. https://doi.org/10.1109/ACCESS.2024.3452426

Liu, W. J., Ge, Y. B., & Gu, Y. C. (2024). News-driven stock market index prediction based on trellis network and sentiment attention mechanism. Expert Systems with Applications, 250, Article 123966. https://doi.org/10.1016/j.eswa.2024.123966

Liu, Y., Hu, T., Zhang, H., Wu, H., Wang, S., Ma, L., & Long, M. (2024). iTransformer: Inverted transformers are effective for time series forecasting. In Proceedings of the International Conference on Learning Representations (ICLR).

Liu, Y., Zhang, H., Li, C., Huang, X., Wang, J., & Long, M. (2024). Timer: Generative pre-trained transformers are large time series models. In Proceedings of the 41st International Conference on Machine Learning (Vol. 235, pp. 32369–32399). PMLR.

Mu, S., Liu, B., Gu, J., et al. (2024). Research on stock index prediction based on the spatiotemporal attention BiLSTM model. Mathematics, 12(18), Article 2812. https://doi.org/10.3390/math12182812

Mutinda, J. K., & Geletu, A. (2025). Stock market index prediction using CEEMDAN-LSTM-BPNN-decomposition ensemble model. Journal of Applied Mathematics, 2025, Article 7706431. https://doi.org/10.1155/jama/7706431

Nie, Y., Nguyen, N. H., Sinthong, P., & Kalagnanam, J. (2023). A time series is worth 64 words: Long-term forecasting with transformers. In Proceedings of the International Conference on Learning Representations (ICLR).

Rasul, K., Ashok, A., Williams, A. R., Ghonia, H., Bhagwatkar, R., Khorasani, A., Darvishi Bayazi, M. J., Adamopoulos, G., Riachi, R., Hassen, N., Bilos, M., Garg, S., Schneider, A., Chapados, N., Drouin, A., Zantedeschi, V., Nevmyvaka, Y., & Rish, I. (2023). Lag-Llama: Towards foundation models for probabilistic time series forecasting. arXiv preprint arXiv:2310.08278.

Shi, Z. (2024). MambaStock: Selective state space model for stock prediction. arXiv preprint arXiv:2402.18959.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48(1), 1–48. https://doi.org/10.2307/1912017

Vaswani, A., Shazeer, N., Parmar, N., Uszkoreit, J., Jones, L., Gomez, A. N., Kaiser, Ł., & Polosukhin, I. (2017). Attention is all you need. In Advances in Neural Information Processing Systems 30 (pp. 5998–6008).

Wang, S., Wu, H., Shi, X., Hu, T., Luo, H., Ma, L., Zhang, J. Y., & Zhou, J. (2024). TimeMixer: Decomposable multiscale mixing for time series forecasting. In Proceedings of the International Conference on Learning Representations (ICLR).

Woo, S., Park, J., Lee, J. Y., & Kweon, I. S. (2018). CBAM: Convolutional block attention module. In Proceedings of the European Conference on Computer Vision (pp. 3–19). https://doi.org/10.1007/978-3-030-01234-2_1

Wu, H., Hu, T., Liu, Y., Zhou, H., Wang, J., & Long, M. (2023). TimesNet: Temporal 2D-variation modeling for general time series analysis. In Proceedings of the International Conference on Learning Representations (ICLR).

Xu, R. (2025). Modeling and comparing S&P 500, FTSE and SSEC stock price with ARIMA model. Frontiers in Economics and Management, 6(6), 60–69. https://doi.org/10.6981/FEM.202506_6(6).0008

Zhang, J., Ye, L., & Lai, Y. (2023). Stock price prediction using CNN-BiLSTM-attention model. Mathematics, 11(9), Article 1985. https://doi.org/10.3390/math11091985